Story Highlights

- Four in 10 investors say higher rates would hurt their finances

- But 43% of retired investors think higher rates will help them

- Majority of investors expect interest rate hike in next year

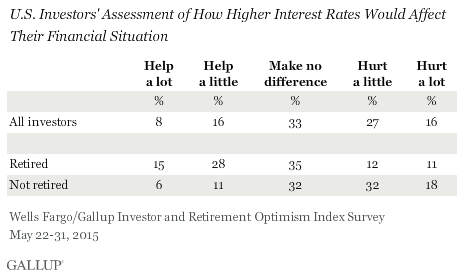

PRINCETON, N.J. -- With the prospect of the first interest rate hike in years still looming, 27% of U.S. investors say higher interest rates would hurt them a little financially, and 16% say it would hurt them a lot. The combined 43% who say higher rates would harm their financial position far outweighs the 24% who say higher rates would help them a little or a lot. One in three say higher rates would not make a difference.

These results are based on the second quarter Wells Fargo/Gallup Investor and Retirement Optimism Index survey, conducted May 22-31, with 1,005 U.S. investors. This survey was conducted before the Federal Reserve opted not to raise rates at its June meeting. For this survey, investors are defined as U.S. adults who have at least $10,000 invested in stocks, bonds or mutual funds, or in a self-directed IRA or 401(k).

While U.S. investors view the prospect of higher interest rates more negatively than positively, this mainly reflects the views of nonretired investors, half of whom say higher rates will hurt them a lot or a little; just 17% say they will help them. By contrast, 43% of retired investors believe higher rates will improve their financial situation while 23% say they will harm it.

Past Wells Fargo/Gallup research provides some insights into why retirees are so concerned about interest rates:

- In 2014, one-third of retirees (34%), versus 24% of nonretirees, reported having certificates of deposit (CDs), likely making retirees more sensitive to the low rates recently associated with these savings instruments.

- Earlier this year, Wells Fargo/Gallup found half of retirees saying that CDs and other types of savings accounted for at least a minor part of their retirement income.

- In 2013, 26% of retirees said low interest rates were forcing them to assume more risk with their investments than they would otherwise.

- In the same poll, 14% of retirees said low rates made it necessary for them to work part time.

- Only 13% of retired investors in 2013, compared with 39% of nonretired investors, said they had recently taken advantage of low interest rates to refinance the mortgage on their home.

The nation's central bank has not raised interest rates since 2006, and Federal Reserve Board Chair Janet Yellen has indicated that while she thinks rates should go higher this year, it will be done slowly and only if the labor market and broader economy improves. One member of the Fed board recently said there is a 50% chance he'll back a rate increase in September.

Investors See More Upside Than Downside in Low Rates

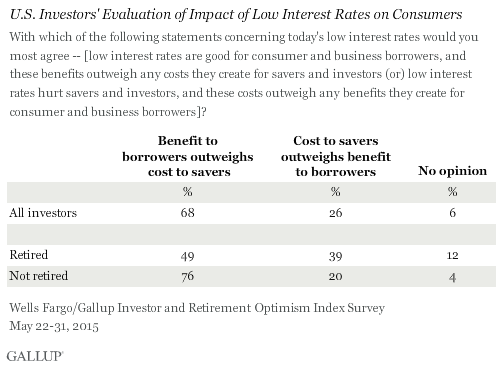

While the Fed's policy of low interest rates is controversial in some political and economic circles, the majority of investors (68%) say the benefit of low interest rates to consumer and business borrowers outweighs any costs they create for savers and investors.

An increasing majority of investors are braced for interest rates to rise. Sixty-one percent in May, up from 56% in February, expect interest rates to go up a lot or a little over the next 12 months. Few -- just 7% -- think rates will go down while about three in 10 expect them to stay the same.

Investor Optimism Holds at Seven-Year High Point

Although Yellen does not believe the economy is showing sufficient strength to raise interest rates right now, investor confidence in 2015 continues to register at the highest level in seven years. The overall Wells Fargo/Gallup Investor and Retirement Optimism Index was +70 in this quarter. That is similar to the +69 index score in the first quarter, but up from +29 a year ago and is the highest since October 2007. Still, the index remains far from its historical high of +178, recorded in January 2000, and has not exceeded +100 since January 2007.

Notably, the stability in investor confidence between the first and second quarters of this year contrasts with the slight decline in Americans' confidence in the economy over the same period as seen in the Gallup Economic Confidence Index. This is likely related to investors' greater exposure to the stock market, which has continued to break records all year.

Bottom Line

For those retirees who financially depend on interest income from savings accounts or CDs, or who want to purchase annuities, today's low rates have been challenging. On the other hand, for working homeowners who have been able to realize huge savings by refinancing their existing home or buying a new home, they have been a financial lifeline.

Those realities are evident in the Wells Fargo/Gallup finding that retirees are more inclined to view low rates in negative terms while nonretirees tend to view them positively. But, in line with the Fed's decision to keep rates near rock bottom for now, both groups believe that, on balance, low rates do more good than harm for consumers as a whole. With investor optimism improving to its highest level in seven years, investors may be getting closer to the point that they can tolerate a rise in interest rates along with the temporary volatility in stocks and bonds it will likely trigger. But with investor confidence still well below the +100 mark, they may not be there quite yet.

Survey Methods

Results for the Wells Fargo/Gallup Investor and Retirement Optimism Index survey are based on questions asked May 22-31, 2015, on the Gallup Daily tracking survey, of a random sample of 1,005 U.S. adults having investable assets of $10,000 or more.

For results based on the entire sample of investors, the margin of sampling error is ±4 percentage points at the 95% confidence level.

In addition to sampling error, question wording and practical difficulties in conducting surveys can introduce error or bias into the findings of public opinion polls.

Learn more about how the Wells Fargo/Gallup Investor Optimism and Retirement Index works.